Angola’s residential rental market entering 2026 is best understood through three lenses:

- Oil-driven macroeconomics

- Dollar-linked upper-tier leasing

- Reform-led structural transition

Unlike diversified rental markets such as South Africa, Angola’s formal residential sector is deeply correlated with hydrocarbon revenues, foreign corporate presence, and currency cycles.

Yet within this volatility lies opportunity. For disciplined investors who understand Angola’s currency structure, legal framework, and corporate leasing ecosystem, the rental market offers selective high-yield income potential, particularly in Luanda’s premium nodes.

This is not a broad-based rental story. It is a concentrated, energy-linked income market.

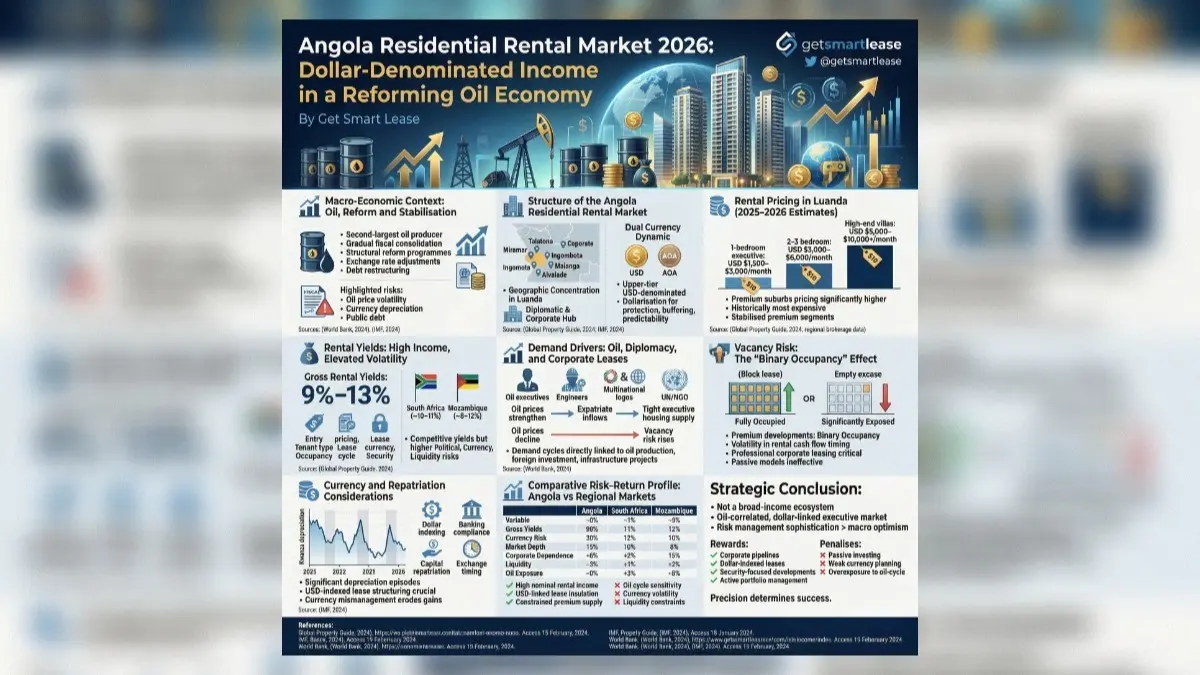

1. Macro-Economic Context: Oil, Reform and Stabilisation

Angola remains Sub-Saharan Africa’s second-largest oil producer. Hydrocarbon revenues continue to underpin fiscal stability, foreign exchange reserves and overall economic growth (World Bank, 2024).

Recent macro trends indicate:

- Gradual fiscal consolidation

- Structural reform programmes

- Exchange rate adjustments

- Debt restructuring efforts

However, Angola remains exposed to:

- Oil price volatility

- Currency depreciation pressures

- Public debt sustainability concerns

(IMF, 2024)

Economic growth is projected to stabilise as reforms progress, but oil dependency continues to define the country’s risk profile.

For property investors, this means rental performance is indirectly linked to:

- Oil production levels

- Foreign direct investment

- Corporate hiring cycles

2. Structure of the Angola Residential Rental Market

Geographic Concentration

The formal, high-value residential rental market is overwhelmingly centred in Luanda, particularly in:

- Talatona

- Miramar

- Ingombota

- Maianga

- Alvalade

Luanda functions as Angola’s diplomatic, corporate, and oil-sector headquarters hub (Global Property Guide, 2024).

Secondary cities play a limited role in formal upper-tier residential leasing.

Dual Currency Dynamic

Angola’s rental market operates under a hybrid currency structure:

- Upper-tier leases are often USD-denominated or USD-indexed

- Broader local market leases are denominated in Angolan Kwanza (AOA)

Given historical Kwanza depreciation cycles, dollar-linked leasing has become standard practice in premium developments (IMF, 2024).

This dollarisation provides:

✔ Partial currency protection ✔ Inflation buffering ✔ Improved investor predictability

However, regulatory shifts and repatriation frameworks must be carefully managed.

3. Rental Pricing in Luanda (2025–2026 Estimates)

Rental pricing in premium Luanda suburbs is materially higher than in most Southern African cities:

- 1-bedroom executive apartment: USD $1,500–$3,000/month

- 2–3 bedroom apartment: USD $3,000–$6,000/month

- High-end villas (Talatona/Miramar): USD $5,000–$10,000+/month

(Global Property Guide, 2024; regional brokerage data)

Historically, Luanda has ranked among the most expensive cities globally for expatriate accommodation during peak oil cycles.

While rental levels moderated post-2016 oil downturn, pricing has stabilised in premium segments.

4. Rental Yields: High Income, Elevated Volatility

Gross rental yields in well-positioned Luanda assets are generally estimated between 9% and 13%, depending on:

- Entry pricing

- Tenant type

- Lease currency

- Occupancy cycle

- Security standards

(Global Property Guide, 2024)

These yields are competitive relative to:

- South Africa (~10–11%)

- Mozambique (~8–12%)

However, Angola carries higher:

- Political risk premium

- Currency risk

- Liquidity constraints

Yield must therefore be assessed against volatility exposure.

5. Demand Drivers: Oil, Diplomacy, and Corporate Leases

Angola’s upper-tier rental demand is heavily driven by:

- Oil & gas executives

- Engineering contractors

- Multinational corporations

- Diplomatic missions

- International NGOs

(World Bank, 2024)

Demand cycles are therefore directly linked to:

- Oil production stability

- Foreign investment flows

- Infrastructure project pipelines

When oil prices strengthen, expatriate inflows increase, tightening Luanda’s executive housing supply.

When oil prices decline, vacancy risk rises sharply.

This creates cyclical compression and expansion patterns not typically seen in diversified markets.

6. Vacancy Risk: The “Binary Occupancy” Effect

Like Mozambique, Angola exhibits what can be termed “binary occupancy risk”:

Premium developments are often:

- Fully occupied under corporate block leases OR

- Significantly exposed during energy downturns

This creates volatility in rental cash flow timing.

Professional corporate leasing relationships are therefore critical.

Passive, retail-focused leasing models are generally ineffective in Luanda’s upper-tier market.

7. Currency and Repatriation Considerations

The Angolan Kwanza has experienced significant depreciation episodes over the past decade (IMF, 2024).

Investors must consider:

- USD-indexed lease structuring

- Banking compliance frameworks

- Capital repatriation processes

- Exchange rate timing

Currency mismanagement can materially erode nominal yield gains.

In Angola, currency strategy is as important as property selection.

8. Comparative Risk–Return Profile: Angola vs Regional Markets

VariableSouth AfricaMozambiqueAngolaGross Yields~10–11%~8–12%~9–13%Currency RiskModerateElevatedElevatedMarket DepthDeepThinThinCorporate DependenceModerateHighVery HighLiquidityStrongerLimitedLimitedOil ExposureIndirectIndirectDirect

Angola offers:

✔ High nominal rental income ✔ USD-linked lease insulation ✔ Constrained premium supply

But carries:

✖ Oil cycle sensitivity ✖ Currency volatility ✖ Liquidity constraints

Strategic Conclusion

Angola’s residential rental market in 2026 is not a broad-income ecosystem.

It is an oil-correlated, dollar-linked executive housing market.

For experienced cross-border investors, Luanda’s premium segment offers strong headline yields and USD income potential.

However, this is a market where: Risk management sophistication > macro optimism.

The Angolan rental sector rewards:

✔ Corporate tenant pipelines ✔ Dollar-indexed lease structuring ✔ Security-focused developments ✔ Active portfolio management

It penalises:

✖ Passive investing ✖ Weak currency planning ✖ Overexposure to oil-cycle optimism

Precision-> not speculation -> determines success in Angola.

References

Global Property Guide (2024) Angola Property Market Analysis. Available at: https://www.globalpropertyguide.com (Accessed: 01 February 2026).

International Monetary Fund (IMF) (2024) Angola: Article IV Consultation Report. Washington, DC: IMF.

World Bank (2024) Angola Economic Update: Reform, Oil and Growth Outlook. Washington, DC: World Bank.

Angola Residential Rental Market 2026: Dollar-Denominated Income in a Reforming Oil Economy